Hybridization is defining the next chapter of energy storage. The US alone will add half a terawatt-hour of new storage between 2026 and 2031 (2.5 times the preceding five years) and an increasing share of that pipeline pairs solar and storage on a shared interconnection[i]. This motion is mirrored across Europe, APAC, and the Middle East as developers race to pair renewables with storage to firm output, capture capacity revenues, and meet offtake requirements.

These hybrid assets are far less forgiving of vendor missteps than standalone storage — and the full cost of that decision is rarely visible until it’s already locked in. This article quantifies what’s actually at stake in year one, and what the right choice makes possible across your entire portfolio.

The Revenue Costs of Choosing the Wrong EMS Vendor

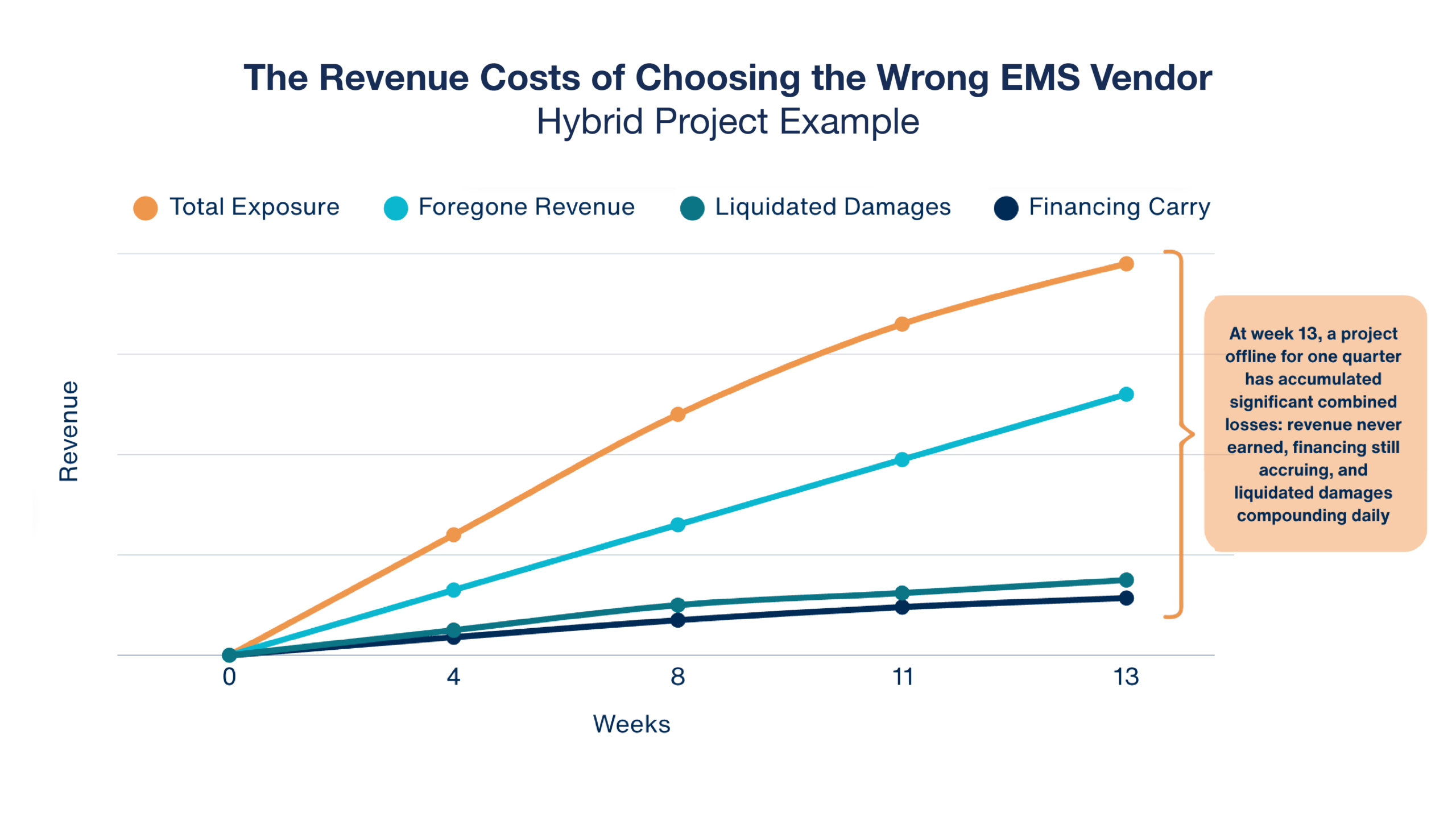

Consider a hypothetical developer who selected an EMS vendor based on cost and familiarity, a reasonable decision at the time. The platform couldn’t coordinate DC-coupled charging, failed interconnection testing, and couldn’t satisfy offtaker requirements. The project sat at 99% mechanical completion for thirteen weeks while the team worked through integration failures the vendor hadn’t encountered before.

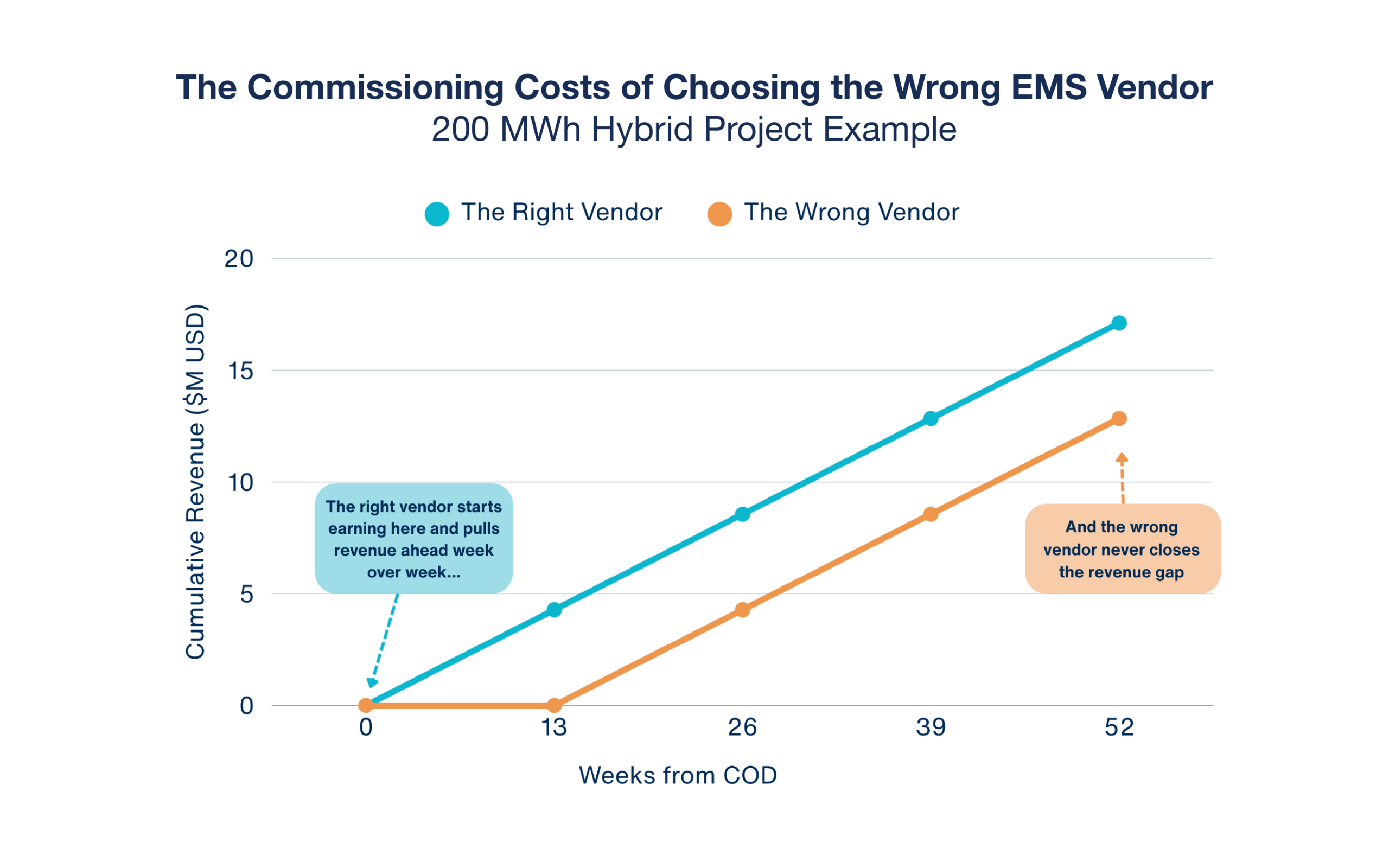

Revenue modeled on CAISO OASIS Day-Ahead Market locational marginal prices, TH_SP15_GEN-APND node, July–September 2025. Assumes 200 MWh hybrid project, 5-hour peak dispatch daily.

The result? Thirteen weeks offline. Millions in losses. And the meter is still running. What makes this number so damaging isn’t its size; it’s that it was never going to show up on a vendor evaluation scorecard. It silently accumulated, week by week, across three categories of loss that compound simultaneously while the project sits idle.

The revenue gap is the starting line for everything that follows. And even stripped down to revenue alone (before financing costs and liquidated damages) the permanent damage is foregone revenue that never comes back.

The Commissioning Costs of Choosing the Wrong Vendor

The wrong vendor might finally come online at week 13, but they start millions behind in foregone revenue and stay there. In the CAISO market, where SP15 peak evening prices averaged $47/MWh in the most recent summer season, that gap is calculable. On a 200 MWh hybrid project dispatching into peak windows, roughly $329K in revenue would be lost every week the project sits idle. No amount of strong performance in the remaining 39 weeks closes it.

By week 52, the wrong vendor has generated $12.84M against the right vendor’s $17.11M, a $4.28M revenue gap that traces back to a single vendor decision made before construction even finished.

By the numbers, it’s clear: the EMS platform you choose today determines whether your portfolio can grow, adapt, and compete as the market keeps moving underneath it.

How the platform you choose today shapes revenue access tomorrow

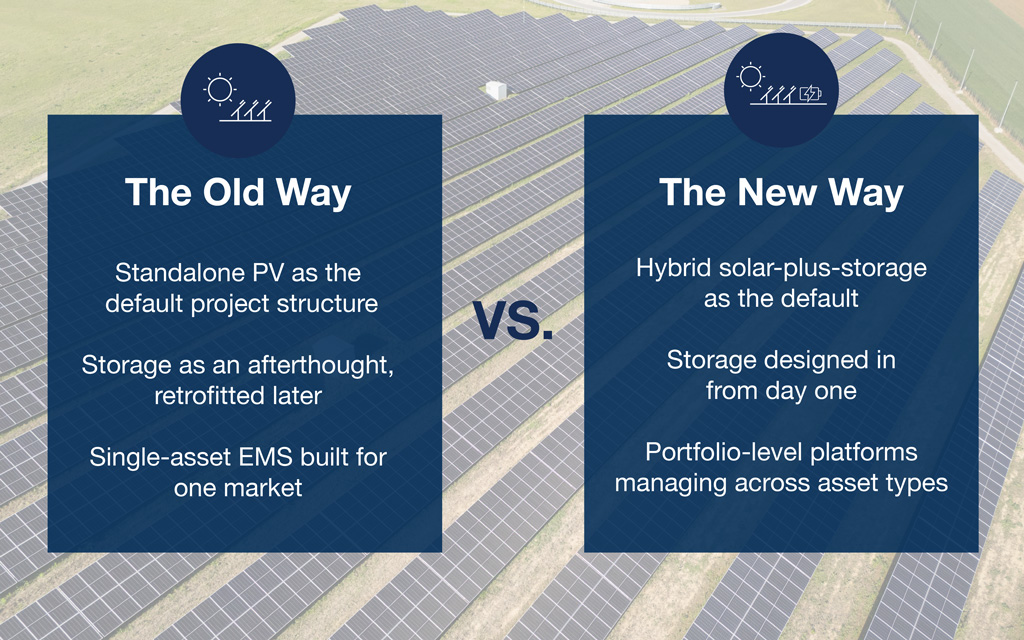

Less than a decade ago, most developers were building standalone solar. Today they’re designing solar-plus-storage from the start. Photovoltaic (PV) asset owners who never planned for storage are retrofitting battery energy storage systems (BESS) onto operational sites because the economics finally make sense. And energy markets keep evolving in ways nobody predicted when many EMS contracts were written.

Proprietary platforms weren’t designed for the hybrid reality. They were designed for a simpler world: one asset type, one market, one vendor relationship assumed to last forever. Now, when the market moves underneath a closed system, asset owners quickly find out what that rigidity costs them.

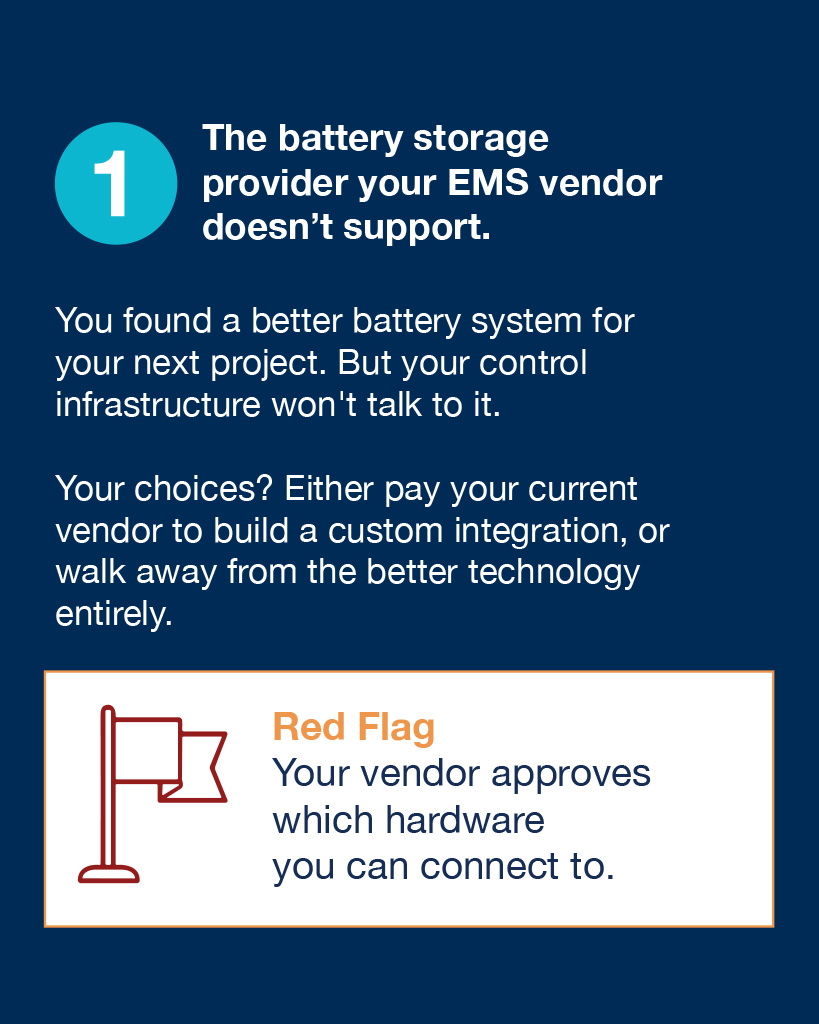

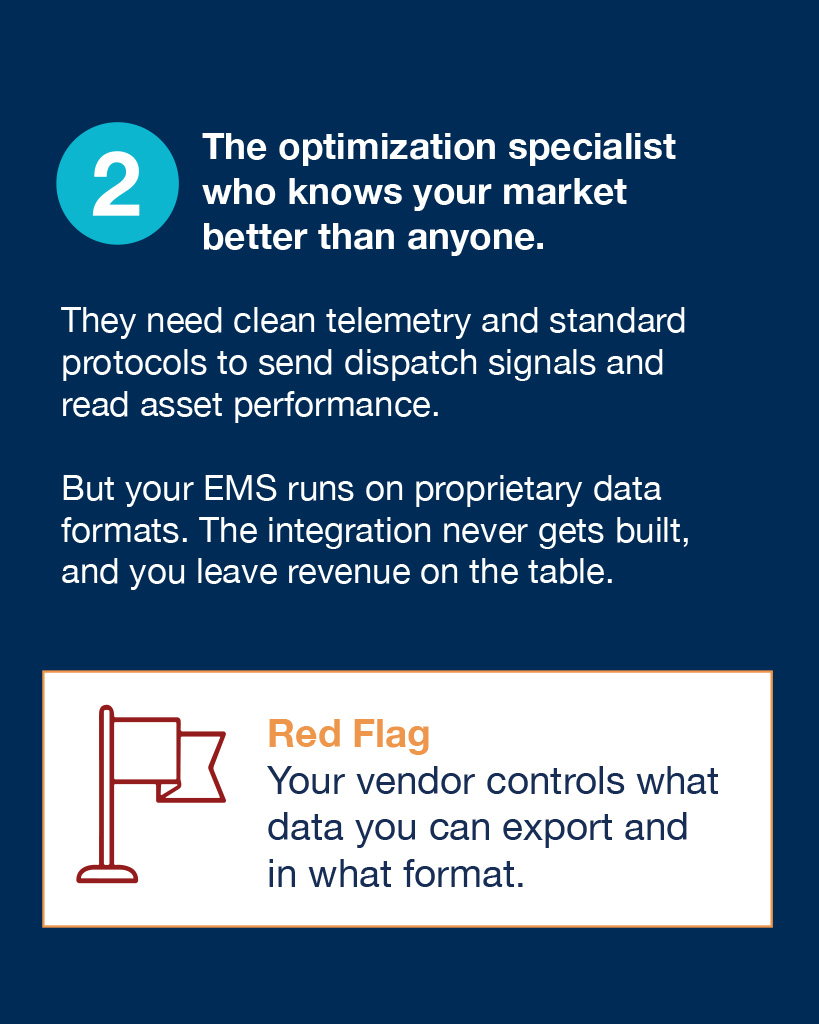

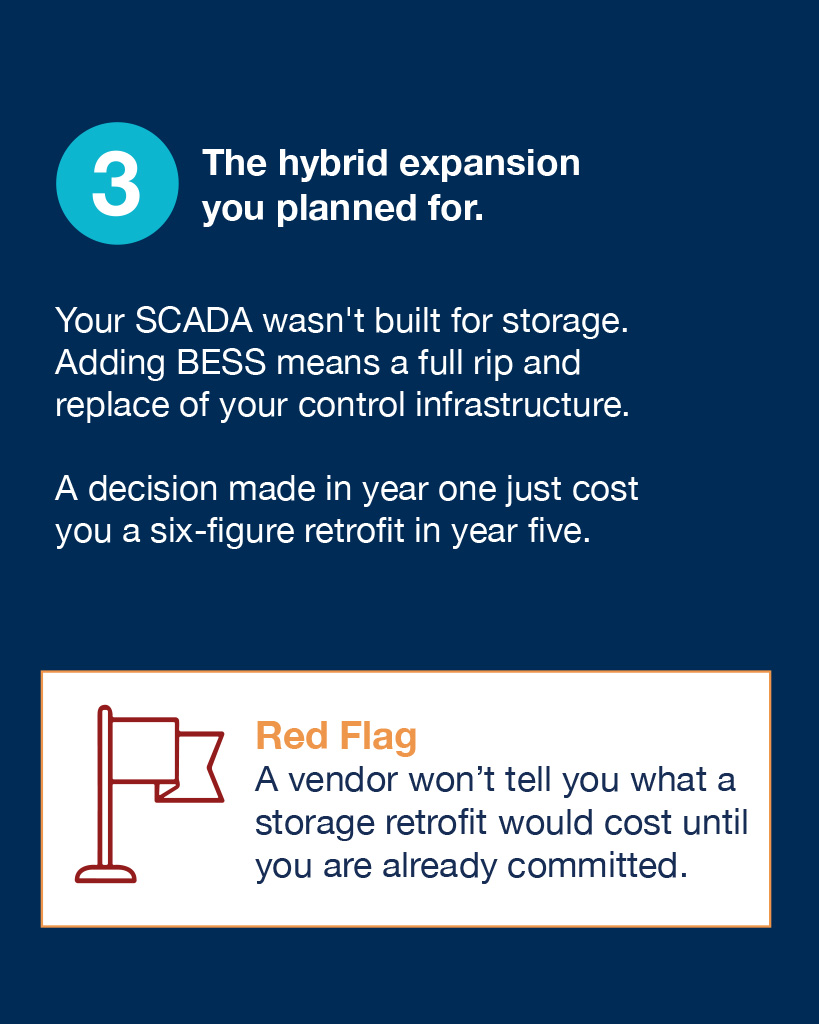

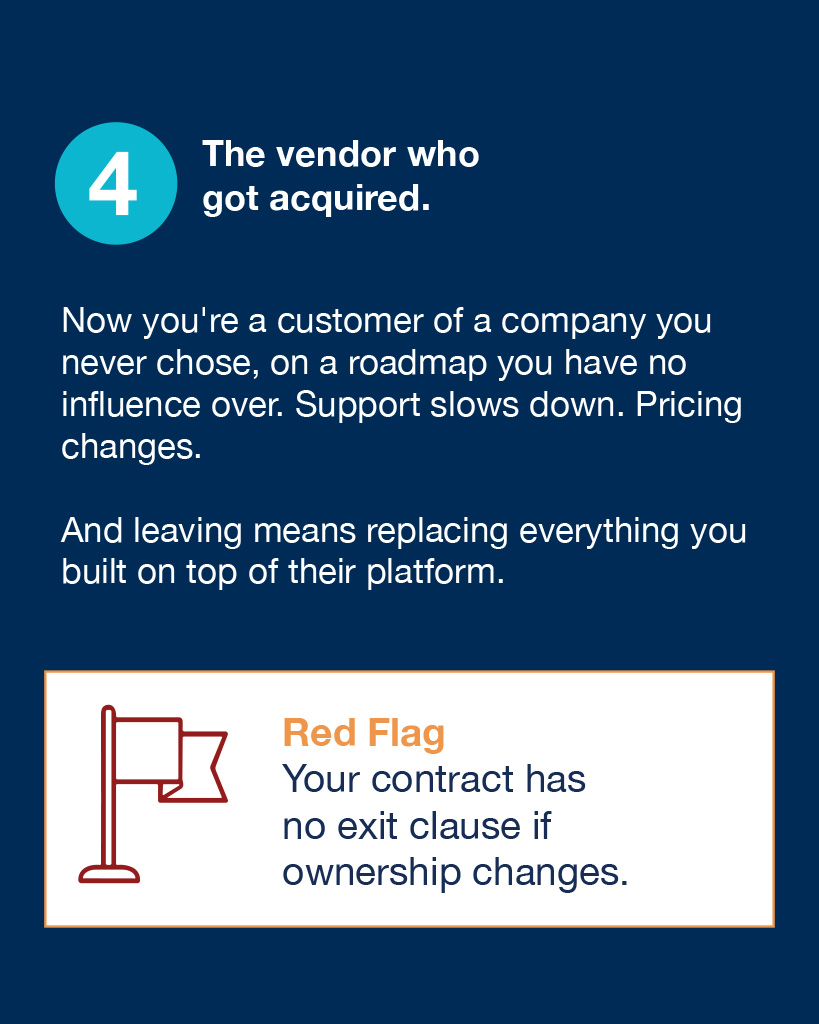

It costs them the storage provider their EMS vendor doesn’t support. It costs them the optimization specialist who knows their market better than anyone but can’t get access to their system. It costs them the upgrade they need when better technology comes along. And when a vendor gets acquired or exits the market, it can cost them everything built on top of that platform.

How an open architecture philosophy unlocks value

PowerTrack EMS was built on the belief that infrastructure should scale with your ambitions, not constrain them. That means separating the stable foundation of monitoring, control, and data from the optimization layer sitting on top of it. Asset owners can integrate best-in-class tools as they emerge, add specialist capabilities where needed, and build their own workflows through APIs, all without starting over.

For asset owners navigating hybridization, open architecture’s real value is immediately apparent. Existing PV sites can add BESS without touching inverters, without replacing hardware, and without retraining teams on a new platform. New hybrid projects get unified control of solar and storage from day one. Sites being built as PV-only today can be ready for storage when the timing is right, without making software decisions now that close off options later.

Across a portfolio, the compounding effect is significant. One interface. Consistent data. The freedom to adopt better tools as they emerge rather than waiting on a vendor roadmap that may never deliver.

The question worth asking before you sign anything

What happens to your portfolio when your platform can’t keep up?

A platform that provides true value doesn’t need the support of contractual walls; it earns for your business by performing, year after year, as your portfolio grows.

After nearly two decades managing solar and storage assets across 55 countries, we’ve seen what lock-in does to portfolios over time. We purpose-built PowerTrack EMS to grow with your portfolio, and we continuously improve our solution to address challenges proactively, as portfolios scale.

Your assets. Your control. Your choice.

[i] Wood Mackenzie Power & Renewables/ACP U.S. Energy Storage Monitor, Q1 2026